Why the Economic Stimulus (Bailout) will

not work.

When we had the gold standard the Congress was only able to

print the exact same amount of currency as there was gold held in the Federal

Reserve at

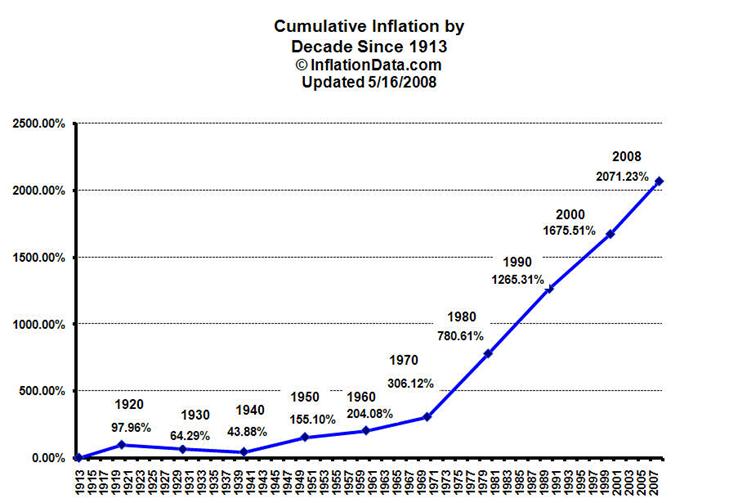

Graph A

Graph B

At the same time due to the influx of new money people who were not eligible to get a loan became eligible to get a credit card, auto loan, and a mortgage. As demonstrated by the second graph while the individual income increased slightly individual debt grew at an alarming pace.

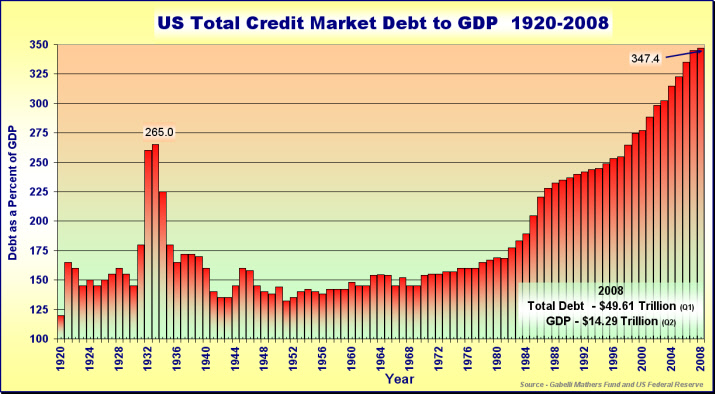

Here is another chart that shows just how bad our debt situation has grown in the last two decades. This next chart shows the ratio of total credit market debt (debt at all levels from household and corporate to government) to GDP. Since 2000 it has grown 25% faster than our economy. This ratio has doubled since 1982.

click to enlarge

Graph C Graph D

Graph C – Total credit market debt to GDP percentage, showing that we hit nearly 350% in the first quarter of 2008. This rate of debt increase is clearly unsustainable but more alarming is what will happen when we have a significant economic slowdown.

As

of the first quarter 2008,

A

similar economic meltdown again, which is now looking increasingly likely,

would push our total debt to GDP ratio to nearly 600%!

According to USA Today and bankrate.com, the average debt of the American household is $84,454 and one out of every 73 of those households had to file for bankruptcy protection in 2003. The average credit card debt is around nine thousand dollars, triple what it was in 1990. Not only are we as a whole getting further in debt, but we aren't saving any money either. Americans are saving just under 2% of their income since 2000, down from an 8% average in the 1980's. What is behind the reasoning for this seemingly careless attitude towards debt and savings in our country? It seems through recent surveys and studies that Kentuckians are going into debt for much the same reasons as the rest of the nation, for necessities. For instance, medical debt is the cause of one in every 20 bankruptcies. The average medical debt for someone that files bankruptcy for that reason is around $25,000. The typical person affected is retired, on a fixed income, and relying on high interest rate credit cards to purchase expensive prescriptions.

If you knew that a $1,000 charge on a credit card would take almost 22 years to pay off, and would cost over $2,300 in interest in you only made the minimum payments would you only make the minimum payments? Most people do. Sixty percent of active credit card debt is not paid off monthly and the typical family pays out about $1200 annually in credit card interest.

Credit

is money wasted and not used to create, generate or support anything. Credit

actually helps to diminish the cash flow while adding to the amount of currency

in the economic environment as most of it goes out in interest. Therefore a Credit Free Life is preferable.